Leveraged Buyout (LBO) Analysis

When one firm is trying to buy another using high amounts of debtLBO is performed when a firm is considering buying another firm with the use of high levels of debt.

Let’s consider an example. Let’s say you have $10. However, you are able to borrow $90 more, so you can invest a total of $100. Now, let’s say you invest that $100 and you earn 10% return on it (goes up to $110). After you repay your debt of $90, you are left over with $20, which is twice as much or a 100% return on your original investment of $10.

Leverage buyouts are very similar to this example. Usually a private equity firm targets a company, buys it, improves it, pays down the debt, and then tries to sell it for more money than they bought it for (at least that’s the plan).

In order to have a good buyout, the predictable cash flows are essential. This is why target companies are usually mature businesses, leaders in their industry segments that have proven themselves over time. The analysis part calculates what return is expected on the buyout.

Things to keep in mind

When you’re performing an LBO analysis, you have a few levers to play with:

- Purchase price

- Free cash flows

- Investment period

- Exit multiple

- Amount of debt and terms

Purchase price

Purchase price is an incredibly important component that will essentially determine what kind of return you’ll make on your money.

For example, if you know that you can sell company for $300 million in 5 years, your return will be much better if you paid $100 million than $200 million for it.

Purchase price is usually determined by applying an EV / EBITDA multiple to the company’s EBITDA. For example, if a company has a $20 million EBITDA and is valued at 5.0x, the purchase price for the company would be $100 million.

Free cash flows

Just like in the DCF analysis, we have to calculate future cash flows. However, in an LBO analysis, we will use the levered cash flows, meaning that we will account for the interest paid on debt. Why? Because we need to figure out how much money we have (after all costs, including interest payments) to repay the outstanding debt.

Investment period

Investment period determines the return on our investment. For example, imagine you invest $50 million and you are promised to get $100 million in return. If you get that $100 million next year, your return on investment will be 100%. However if you get that same $100 million in 5 years, your annual return will be approximately 15%.

Exit Multiple

Exit multiple will determine for how much money you can sell the company. If your EBITDA at exit is $50 million and your exit multiple is 6.0x, you will sell your company for $300 million ($50 x 6).

Debt amount and terms

Since in leveraged buyouts you use a lot of debt to purchase the company, it is very important to consider the amount of the debt, how much interest you will be paying for it, how much it will restrict your operations, and how much of it you can repay given your financial projections.

How does it work?

The high-level concept of a leverage buyout is very simple:

Buy a company Improve it or Sell it

In terms of the analysis, you will need to take the following steps:

1. Determine the purchase price

As mentioned above, purchase price is usually determined by applying an EV / EBITDA multiple to the company’s EBITDA. For example, if a company has a $20 million EBITDA and is valued at 5.0x, the purchase price for the company would be $100 million.

2. Determine how much debt you’re going to use

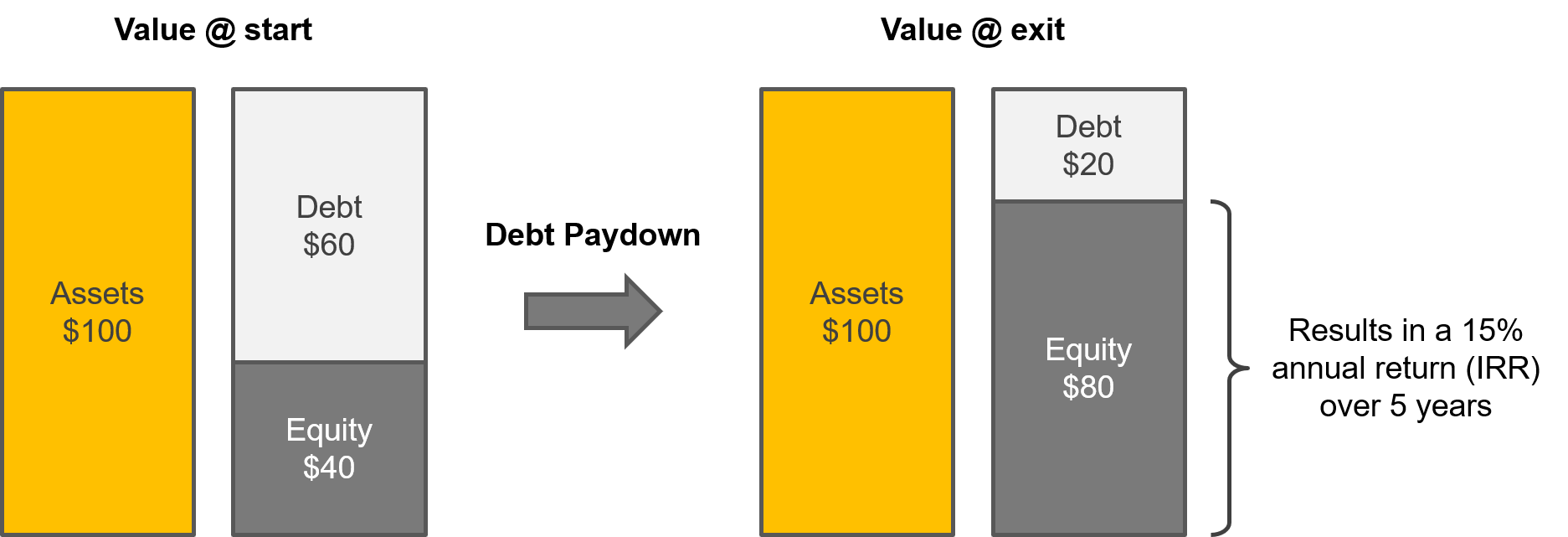

In a typical LBO transaction, you will use about 60% of debt and 40% of equity. In the example above, you would borrow $60 million from the bank and pay $40 million out of your own pocket (equity).

Most times, private equity firms and large investment banks (the lenders) think of leverage in terms of “turns of EBITDA”. Simply put, they want to know how many years’ worth of cash flow (or EBITDA) will it take to pay down the entire balance of the debt. Typically, most leveraged buyout transactions will remain below the 6.0x Total Debt/EBITDA. This means that is the company produces the same amount of EBITDA every year, it will pay off the debt in 6 years.

Additionally, investment banks usually make private equity firms pay a minimum amount of equity or cash out of their own pockets. The banks do this to ensure that the private equity firm also has some downside risk if the investment goes wrong. Typically, private equity firms are required to pay a minimum of 30% of the transaction price in equity.

3. Project the financials and figure out the free cash flows

4. Determine the exit enterprise value of the investment

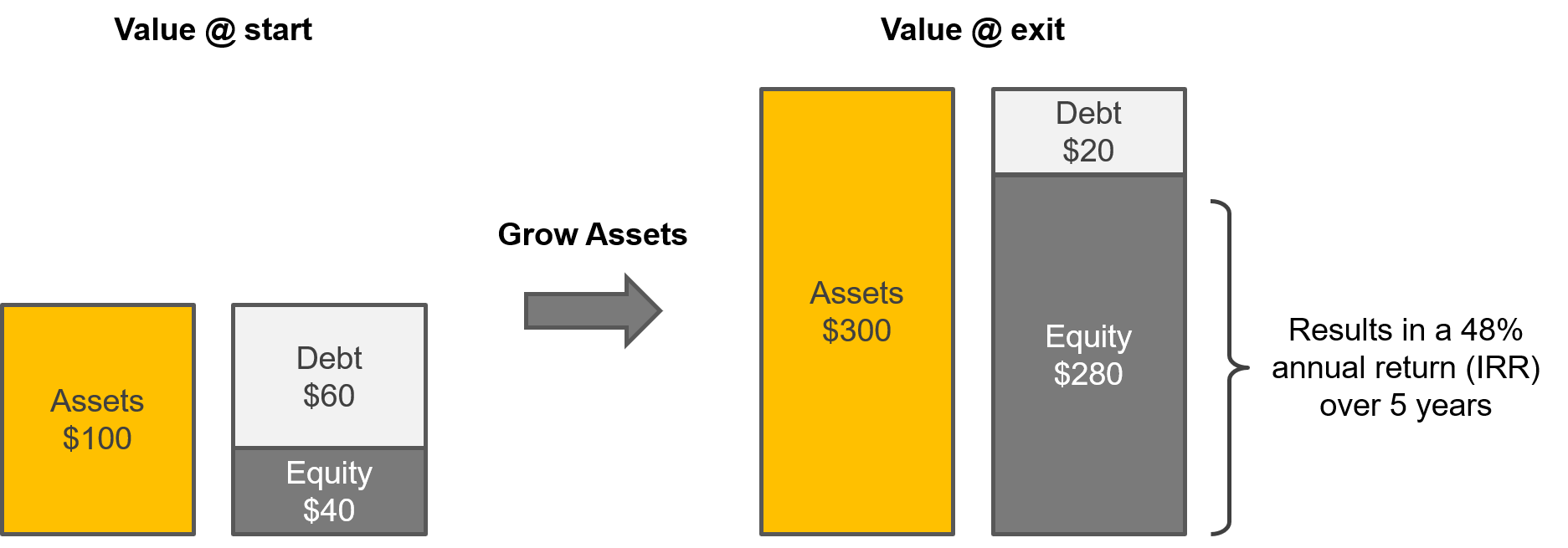

Exit price is determined the same way as purchase price – multiply the final year EBITDA with the respective exit multiple. For example, let’s say you grew original EBITDA from $20 million to $30 million, and since you improved the business, you also get an exit multiple of 6.0x EV / EBITDA (vs. 5.0x purchase multiple). Now the enterprise value of the company is $300 million (6 x $50 million).

5. Subtract the remaining debt and add cash in order to come up with the final equity value

Even though you can sell your business for $300 million, it doesn’t mean that that is the equity value of the investment. In order to come up with the equity value, you need to subtract the remaining debt and add all the cash you accumulated during the time of the investment.

For example, let’s say we repaid $40 million of the original debt (which means you still owe $20 million) and generated zero extra cash. Your implied equity value would be $300 – $20 + $0 = $280 million.

6. Compare the initial equity amount to the exit equity amount

You originally invested $40 million of equity and five years later, after repaying all the outstanding debt and accounting for all the extra cash that the business generated, you have $280 million in equity.

That means that you made 7.0x your original investment or 48% annual return (given the investment period of 5 years). Private equity firms typically expect at least 20% in annual returns in order to justify any given investment.

And here are examples of why private equity firms are doing it: